Excerpt:

"Key takeaways:

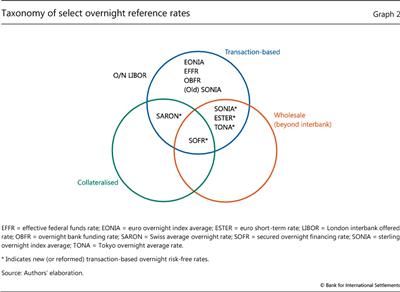

- The new risk-free rates (RFRs) provide for robust and credible overnight reference rates, well suited for many purposes and market needs. In the future, cash and derivatives markets are expected to migrate to the RFRs as the main set of benchmarks. The transition will be most challenging for cash markets because of the bespoke nature of contracts and structurally tighter links to interbank offered rates.

- To manage asset-liability risk, financial intermediaries may continue to need a set of benchmarks that provide a close match to their marginal funding costs - a feature that RFRs or term rates linked to them are unlikely to deliver. This may call for RFRs to be complemented with some form of credit-sensitive benchmark, an approach already undertaken in some jurisdictions.

- It is possible that, ultimately, a number of different benchmark formats will coexist, fulfilling a variety of purposes and market needs. The jury is still out on whether any resulting market segmentation would lead to material inefficiencies or could even be optimal under the new normal."

Image credit - Schrimpf and Sushko, 2019

No comments:

Post a Comment